Volatility matters

A more detailed look at how volatility is approached in the back-test

Volatility plays a central role in how option traders price contracts.

Here’s how we dealt with volatility as a parameter during our back test.

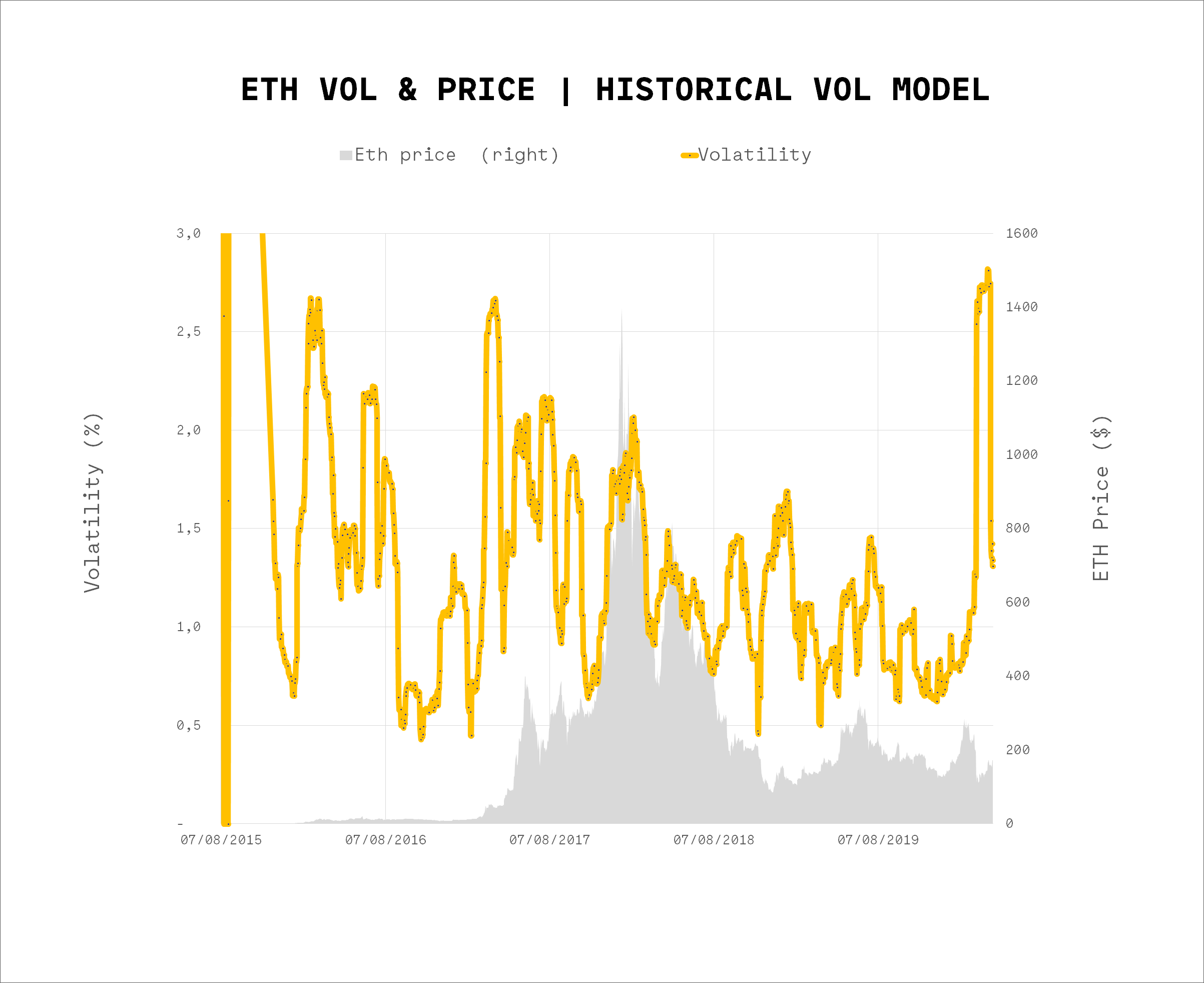

Approach one: historical volatility.

Example: 30 day expiration cycles.

At expiry, I buy a new At the money put.

To price the put, I take the standard deviation of returns over the last 30 days, I annualize them, and I input that into a Black-Scholes engine.

On top of the BS price, I add an additional 20%, to make puts more expensive, and make the model more robust.

This is the resulting volatility:

Note: In the vertical axis, it’s 00s. eg. 1,5 = 150%, 2,0 = 200%, etc.

Approach two: realized volatility.

Example: 30 day expiration cycles.

At expiry, I buy a new At the money put.

To price the put, I take the standard deviation of returns over the next 30 days (since I’m doing a back-test, I actually can look at the volatility ahead), and I input that into a Black-Scholes engine.

On top of the BS price, I add an additional 20%, to make puts more expensive, and make the model more robust.

This is consistent with Implied Vol being uniformly higher than Realized Vol in sampling from VIX on S&P500.

This is the resulting volatility:

As you can see, the realized model shows the same volatility as the historical model, just shifted 30 days. In the realized volatility model, volatility is “perfectly” priced ahead of time, whereas historical vol method is just delayed.

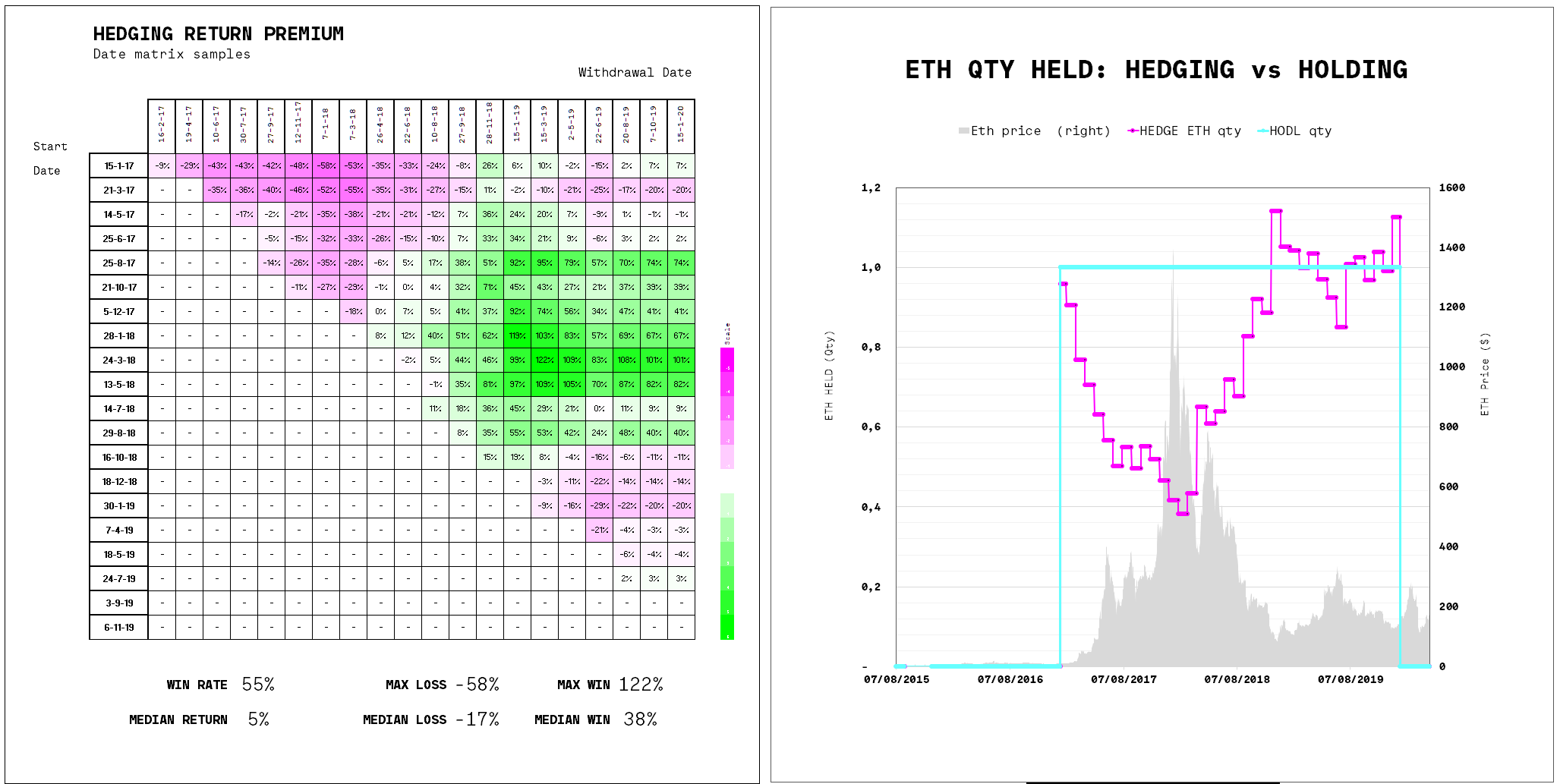

Impact on results

Let’s look at the same period and parameters, run with both Historical and Realized Volatility models.

Realized

Historical

Results are quite similar. This was unexepcted to us, but it seems to indicate that price action is a much bigger driver for actual returns.

I know option pricing is a very heated space - interested in hearing people’s thoughts about the approach, and possible alternatives/ideas, to produce the most reliable results possible.